OK so Kiwi investors are

finally cottoning on to this SaaS game, right? Xero, SLI Systems, Vend, GeoOps, Diligent... - all subscription-based recurring revenue businesses with strong management teams, happy customers and consistent growth. But often not profitable, no sign of a dividend for years to come - a concept that until recently was just alien to traditional NZ investment community.

Yet Xero is now up there on the market cap leader board on the NZX -

recently just over NZ$5Bn - and still hasn't made a profit. Their

most recent interim report states that the company is "continuing to follow a growth agenda focused on creating longer-term shareholder value rather than short-term profitability".

In all likelihood with businesses like this, there are only three possible options for shareholders to realise their gains:

A) Trade sale to a bigger international player.

B) IPO (if it hasn't been done already)

C) Hang around until the company reaches a growth inflection point, stops burning cash on R&D and Marketing, farms their customers for 7+ years and starts paying a regular dividend

You'd have to be a very loyal shareholder to wait for Option C. So what's going on with the valuation?

I thought I'd just run the numbers and see how the - let's face it, *exuberant* - valuations of some Kiwi SaaS companies compares against recent international (mainly US) research and commentary.

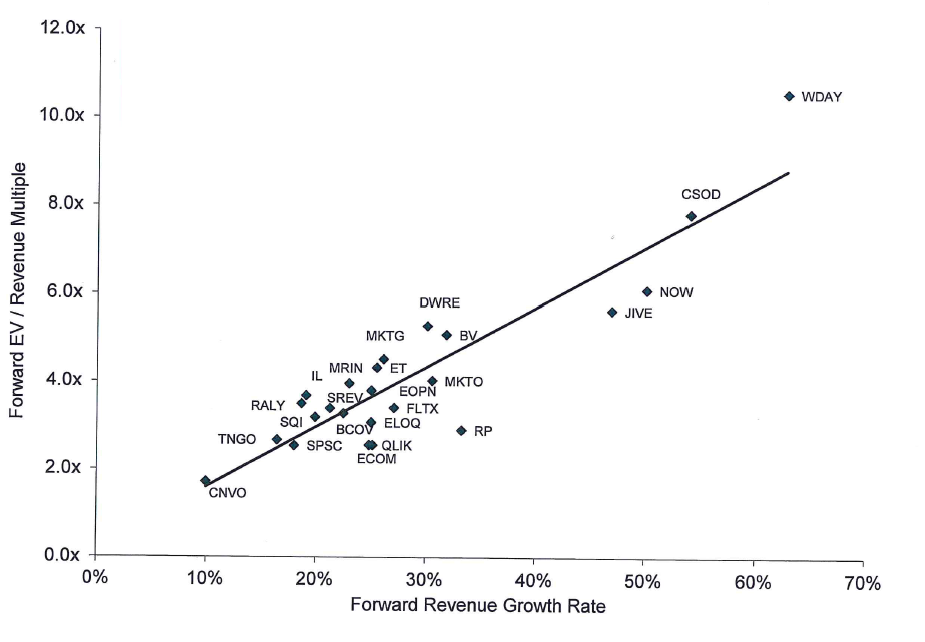

There are three good jumping off points that I've found from the last year which discuss valuation dynamics of recurring-revenue (SaaS) businesses. All three point to Revenue Growth Rate as being the primary - but not only - determinant of valuation multiple:

Dave Kellogg is the CEO of

Host Analytics, a cloud-based enterprise performance management (EPM) vendor.

Forward revenue valuation multiple = (Growth rate % / 10) + 1

(Source: David Kellogg)

Valuation = (2*ARR) + (ARR*(1+(GRM*GR)))

(ARR = Annual Recurring Revenue, GRM = Growth Rate Multiplier (assume ~ 2.5), GR = Growth Rate)

(Source: SaaS Capital)

Again, a clear correlation between revenue growth and valuation multiple. (Check out the whitepaper What's Your SaaS Company Worth that these guys have published as well - a pretty comprehensive framework which includes other factors including Addressable Market Size, Customer Retention, Gross Margin and Customer Acquisition Costs(CAC).

So, given these recent analyses how do the handful of NZ SaaS vendors with publicly available data stack up?

I've given it a quick crack and come up with the following figures. Happy to share my workings if anyone's interested - several guesses made around Gross Margin (not all companies report consistently) - that may skew things a bit, but nonetheless the numbers tell a story: when it comes to Kiwi SaaS firms (especially those aligned closely with the Xero ecosystem) there's something in the water. Question is: what is it and who's drinking it?

| Company |

ARR (NZ$) |

ARR Growth % |

Market Cap (NZ$) - Dec 2013 |

Kellogg Multiple |

Cummings Multiple |

Actual Multiple |

| Xero |

$70.6 million (source) |

82% |

$3,900 $4304* million |

9.2 |

5.05 |

55 * 61 |

| SLI Systems |

$19.3 million (source) |

25% (forecast) |

$115 million |

3.45 |

3.61 |

6 |

| Diligent |

$70.3 million (source)(US$58.3 million) |

80% |

$316 million |

9.00 |

5.00 |

5 |

| GeoOps |

$1 million (? 4500 paying users at $20/user/month with churn and discounts?) |

100% (? Charitable guess) |

$53 million |

11.00 (?) |

5.50 (?) |

53 (?) |

* (Doh! use NZ$ not US$)If you're running a SaaS firm and want to run your numbers through the spreadsheet and see how you compare,

get in touch.